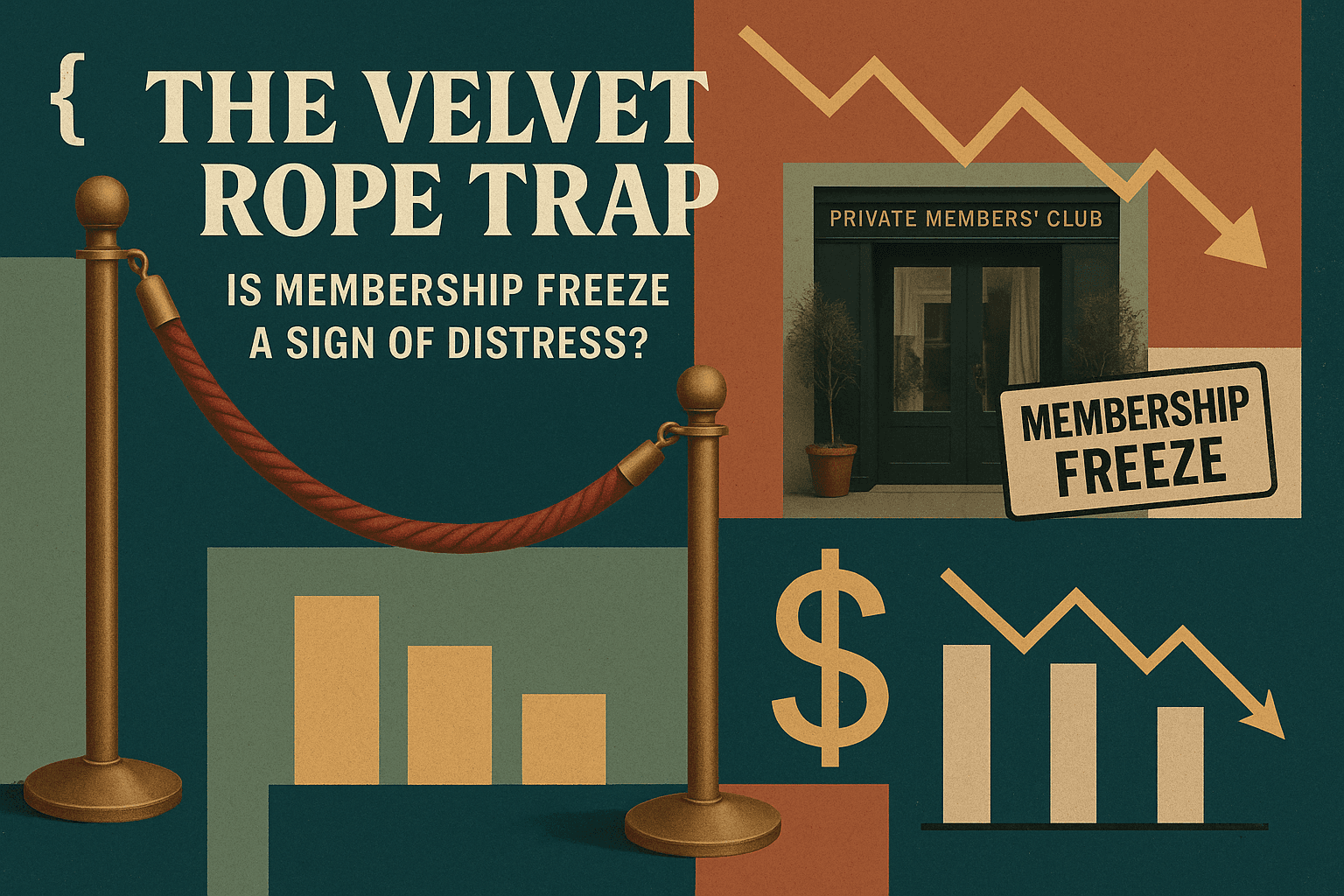

Le Piège du Velours: La Suspension des Adhésions de Soho House est-elle un Signe de Détresse ?

La décision de Soho House & Co de suspendre les nouvelles adhésions dans des marchés clés a suscité le débat. S'agit-il d'un retour à l'exclusivité ou d'un masque pour des défauts opérationnels plus profonds ?

The Analyst

Author

The Analyst

Le Piège du Velours: La Suspension des Adhésions de Soho House est-elle un Signe de Détresse ?

Depuis des décennies, le modèle de club privé prospère sur un principe économique fondamental : la rareté crée de la valeur. Pourtant, l'annonce récente de Soho House & Co de mettre en pause les nouvelles adhésions dans ses marchés clés - Londres, New York et Los Angeles - a suscité une vive division entre l'intention déclarée de l'entreprise et le sous-texte analytique. Alors que le récit corporate présente cela comme un retour stratégique à l'exclusivité, un examen plus attentif suggère que la "suspension des adhésions" pourrait être une mesure réactive pour masquer la saturation du marché et les défauts structurels du modèle économique.

La Position Corporate : Prioriser la Qualité

La décision de suspendre les nouvelles adhésions dans ces hubs critiques a été présentée comme un mouvement délibéré pour protéger l'expérience des membres. Selon le PDG Andrew Carnie, la suspension vise à préserver la "magie" des clubs en évitant le surpeuplement et en maintenant des normes de service élevées [1]. D'un point de vue opérationnel de surface, ce raisonnement semble solide - un fort trafic peut mettre à mal la prestation de services et l'accès aux installations, risquant la satisfaction des membres de longue date. L'entreprise a souligné son engagement à traiter les plaintes des membres concernant l'accès au club et l'atmosphère, affirmant qu'elle "travaille jour et nuit" pour élever les niveaux de service [1].

Le Contrepoint : Un Modèle Sous Tension ?

Sous la rhétorique polie de l'exclusivité se cache une interprétation plus troublante. Un rapport cinglant de GlassHouse Research décrit Soho House & Co comme étant aux prises avec une "crise existentielle", affirmant que la suspension n'est pas un jeu de luxe proactif mais une tentative désespérée de dissimuler un modèle économique défaillant [2]. La critique repose sur la dépendance historique de l'entreprise à l'expansion pour générer des revenus. En plafonnant les adhésions dans ses marchés les plus matures, Soho House & Co étouffe effectivement un flux de revenus clé - un mouvement que les analystes soutiennent masque un point de saturation où le coût d'intégration de nouveaux membres dépasse leur valeur à vie, surtout si les taux de désabonnement non divulgués augmentent [2].

Signes d'Alerte Financière

Peut-être que les préoccupations les plus alarmantes concernent la santé financière de l'entreprise. Les critiques ont examiné ses pratiques comptables, alléguant que ce qui est présenté comme un potentiel de croissance est, en réalité, un fardeau de dette précaire. Le rapport GlassHouse va jusqu'à qualifier les capitaux propres de l'entreprise de "sans valeur", établissant des parallèles avec le modèle malheureux de WeWork, qui s'est effondré sous le poids d'une expansion rapide et d'une économie d'unité insoutenable [2].

Cela soulève une question cruciale : Si la croissance est bloquée dans les marchés clés et que les niveaux d'endettement sont aussi lourds que suggéré, comment Soho House & Co maintiendra-t-elle ses propriétés vieillissantes ? Les analystes avertissent que la structure du capital pourrait être trop fragile pour soutenir une véritable suspension de "contrôle de qualité" sans déclencher des conséquences financières significatives [2].

Implications pour les Parties Prenantes

Pour les investisseurs, la suspension des adhésions signale un potentiel changement d'un récit axé sur la croissance vers un scénario de détresse. Si l'entreprise n'a jamais été véritablement rentable même durant les phases d'expansion - comme le suggèrent certaines analyses - retirer le levier de croissance pourrait exposer des insolvabilités sous-jacentes [2].

Pour les membres, les perspectives sont tout aussi sombres. Bien que la suspension promette une expérience moins encombrée, les pressions financières mises en avant par les analystes laissent entrevoir d'éventuelles mesures de réduction des coûts à l'horizon. Si la théorie du "modèle brisé" se vérifie, les améliorations de service promises pourraient s'avérer non financées, laissant les membres avec un accès exclusif à des actifs en déclin [2].

Un Test de Rorschach du Marché

En fin de compte, la suspension des adhésions sert de test de litmus pour interpréter la trajectoire de Soho House & Co. S'agit-il d'un réajustement calculé pour protéger l'équité de la marque, comme l'affirme l'entreprise [1], ou de l'arrêt brutal d'une entreprise à court de ressources, comme le soutiennent les critiques [2] ? La véritable réponse ne réside pas dans des communiqués de presse polis mais dans la réalité brute du bilan.

Clause de non-responsabilité : Cet article est une publication indépendante. Nous ne sommes pas affiliés à, soutenus par, ou opérés par Soho House & Co. Les informations sont basées sur des sources publiques et des principes d'utilisation équitable pour le commentaire et la critique. Aucun soutien n'est implicite.

Références & Citations

Divulgation Éditoriale

Cet article est une publication indépendante. Nous ne sommes pas affiliés à Soho House & Co. Les informations sont basées sur des sources publiques et des principes d'utilisation équitable pour les commentaires et la critique. Aucune approbation n'est impliquée.